The financing of a new rapid transit project in Toronto is a complex business, and probably the most complex part of the whole thing is the effect this has on property taxes.

This article is intended as an introduction to how these taxes actually work. It is not an exhaustive review, and there are subtleties beyond my scope here.

This is an article for people who like the gory details, and so I will insert the break right here.

Links to Reports

Toronto Council 2016 Budget Presentation

2016 Property Tax Rates and Related Matters

Briefing Note: 2016 Residential CVA Changes

Toronto Council 2015 Budget Presentation

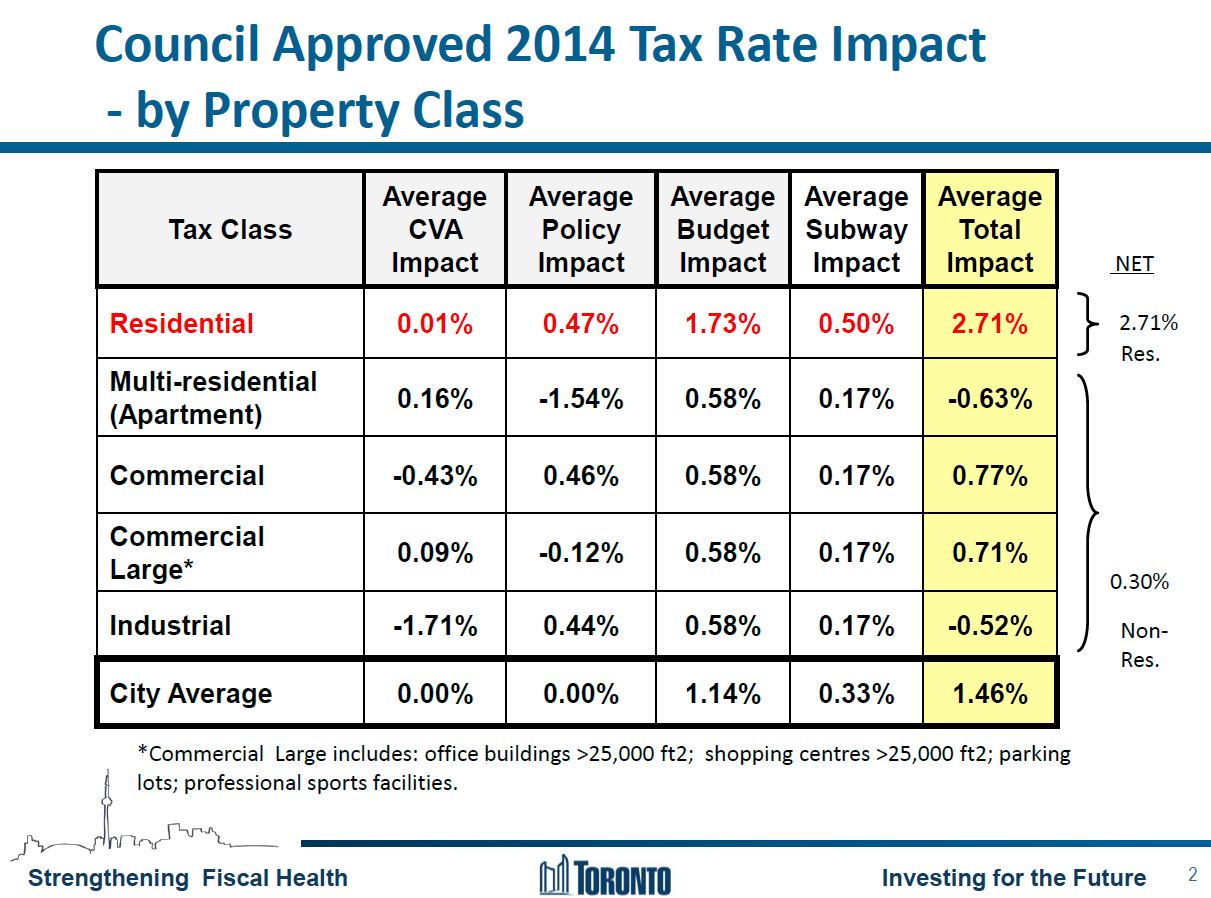

2014 Tax Rate Impacts by Property Class

Scarborough Rapid Transit Options (2013)

The City of Toronto’s Long-Term Financial Direction (May 2016)

2017 Budget Directions & Schedule

Property Tax Classes

There are different types of property for the purpose of taxation, and the rates for each class differ. A house with an assessed value of $1 million pays at a different rate from a commercial building or a factory. There are many reasons for the difference in rates, and a lot of this is buried in the local economic history of any city.

Toronto has long had a strong base of commercial and industrial property, and this has been used to keep taxes relatively low on residential property. The same mechanism was not available to much of the GTHA, and so residential taxes carried a proportionately larger share of the total burden. About a decade ago, after much complaint from businesses in Toronto, the province legislated and Toronto began to implement a “rebalancing” of tax loads among property classes with a view to reaching a similar ratio as in the 905. This has had the effect over time of increasing residential taxes faster than other classes, notably for commercial property which includes multi-unit residential buildings, not just office towers.

The downside to this scheme is that homeowners do not care about rebalancing, only about having the lowest possible taxes. When politicians say “we will hold your tax increase to inflation”, this does not quite mean what it says because a good chunk of the residential property tax increase is actually caused by an offsetting decrease in taxes on other types of property. When the total increase is kept low, there is less headroom for truly inflation-based increase in revenue. This process has been underway for several years and is expected to be completed by 2020.

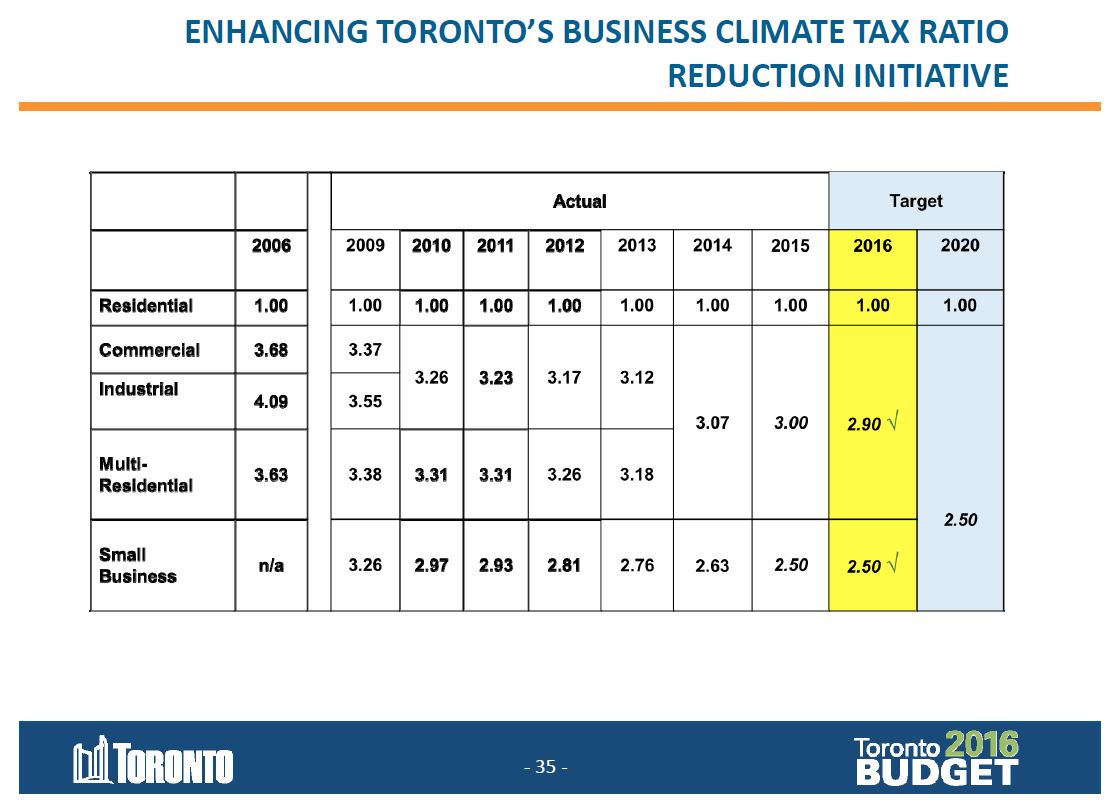

The target level is to have non-residential tax rates at 2.50 times the residential rate by 2020. This had already been achieved for the Small Business rate in 2015, and the other classes now sit at a ratio of 2.90. This is expected to drop by 0.10 in each of the next four years.

The actual machinery of this shift is accomplished through two separate processes:

- Any tax increase is applied on a 3:1 ratio between the residential class and all others. This means that if someone says “taxes are going up by 2%”, they are actually going up 3% on residential and 1% on the rest. In recent years, the focus has been on the residential increase, and so when the statement is “your taxes are going up by 2%”, this is the residential change, and other classes only see a 0.67% bump (1/3 of residential).

- Other tax policies trigger a shift of some non-residential tax load to residential properties each year. Because this represents a decrease for non-residential, the combined effect even if taxes go up overall can be that some property classes actually see a tax reduction.

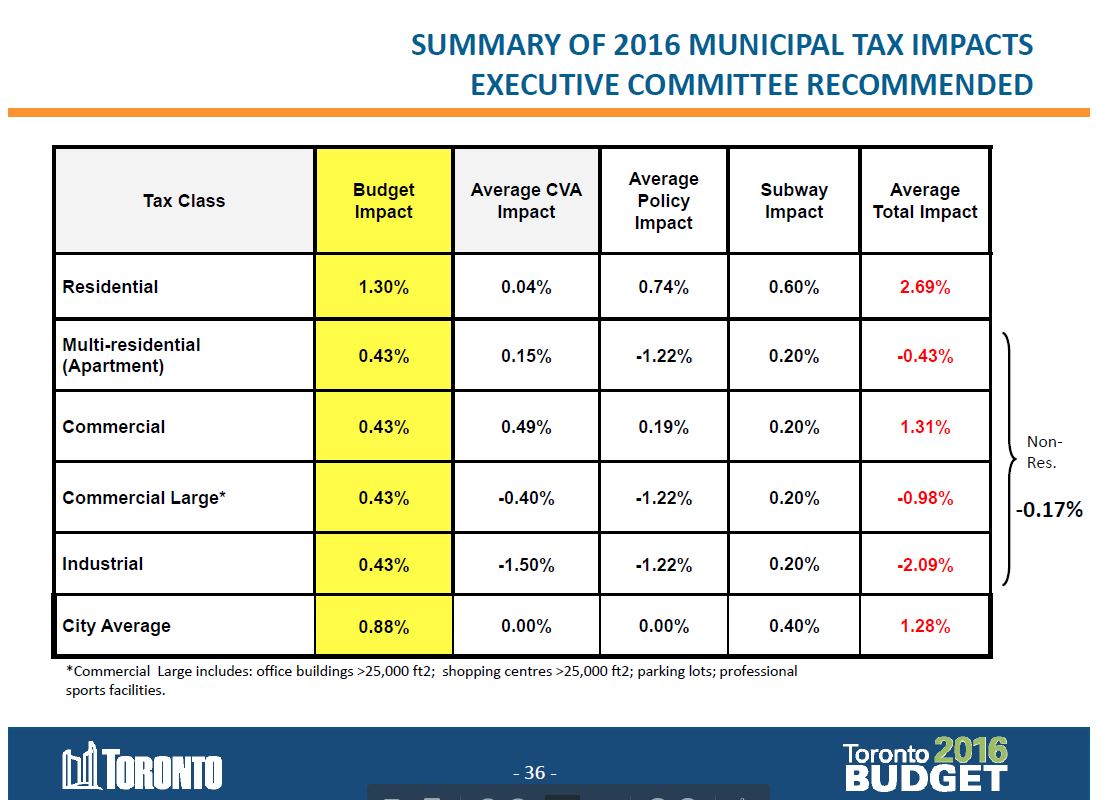

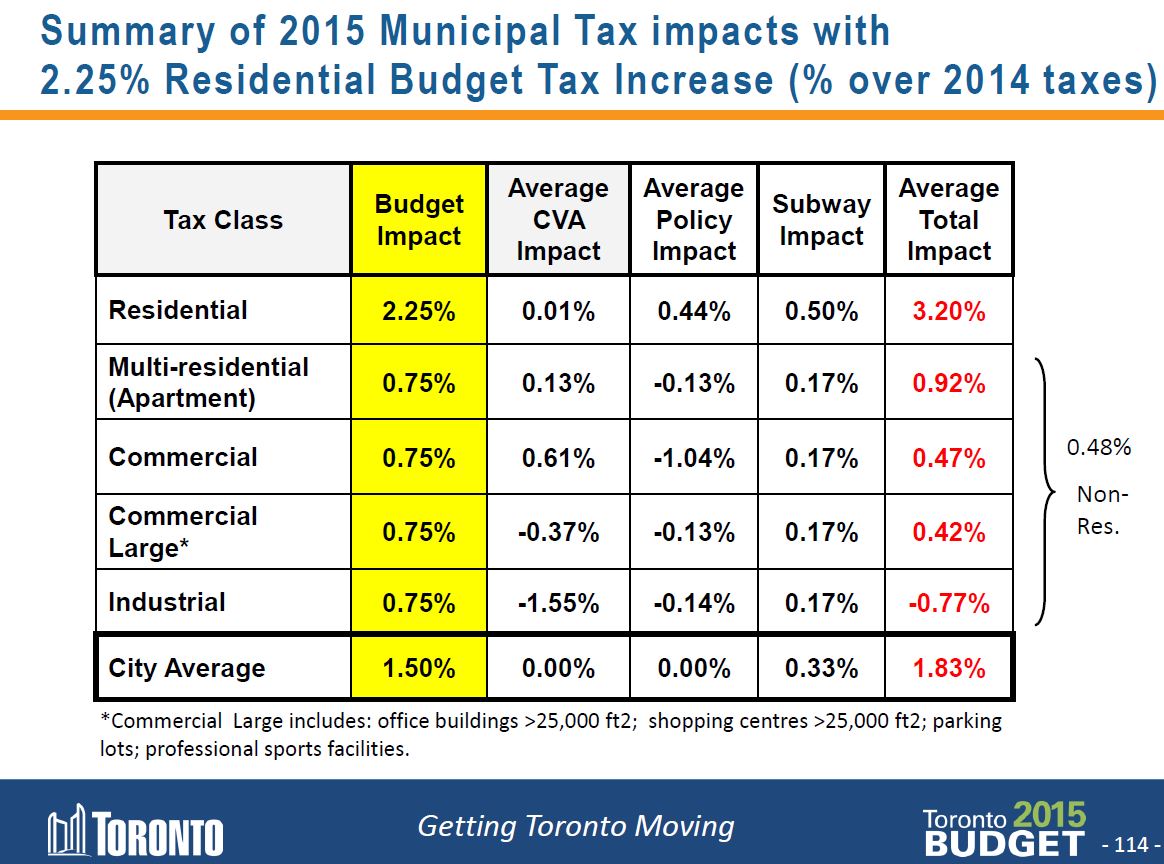

The actual rates of tax increase for 2016 are shown below.

For 2016, non-residential tax rates actually went down 0.17% while residential rates went up 2.69%. The components of these changes are in each column above.

- Budget impact: The city decided to increase residential taxes by 1.30%, with a corresponding 0.43% non-residential change. Note that the effect over the entire city was to bring in less than 1% more revenue. This approach has been a drag on city revenues for several years.

- CVA Impact refers to the shifting of tax loads among property classes due to differences in the value of each type of property. Some classes went up, while others went down. The underlying values come from Current Value Assessment which is explained in more detail below. By law, the effect of CVA changes must be revenue-neutral, and so the city average for this column is zero.

- Policy Impact refers to the “other” policies causing shifts between property classes. Because these policies only move tax charges between property classes, the overall effect is revenue-neutral.

- Subway Impact is the imposition of a 0.6% tax increase for the Scarborough Subway Extension (SSE). Note that the actual increase across the city is only 0.4% because non-residential bears a lower increase.

The amount of tax collected is also affected by the amount of taxable property available. Taxes on a typical residence may go up by 2.69%, but if there are more residences, these bring new revenue.

Not shown in the table above is the effect of appreciation in property values, and this is picked up by the CVA machinery.

Current Value Assessment

On a four year cycle, the Municipal Property Assessment Corporation (MPAC), an entity created by the province, updates the assessed value for taxes of every property in Ontario. The basic premise behind property taxes is that every owner should pay based on the value of their property, and a pre-requisite to that is that the values must be calculated on a consistent basis. In a “hot” market like Toronto’s where the values may have nothing to do with an owner’s personal wealth, but rather with speculative pressures and turnover, this premise has its flaws, but I am not going to debate them here.

Toronto is at the beginning of a cycle, and updated valuations have just been issued for all residential properties. Over the past four years, the average value of residential property has risen by 7.5% annually. If the city were frozen in time, and there were no units added or demolished over the period, then the total assessed value for the city would have gone up 30% (actually the value is slightly higher due to compounding). To maintain revenue-neutrality, taxes would go down by a corresponding amount so that the revenue they generate would stay the same in a no-tax-increase scenario. For example, a house assessed at $500,000 would now be worth $650,000. It might still be taxed at $2,500 (say), but the rate of tax would be lower to match the higher value.

That’s the simple version, but the real world is much more complex.

- Property values change by different amounts depending on where a residence is located, what type of dwelling it is (detached house, condo, etc), and whether there have been any improvements (new rooms, major renovations).

- New housing is built and old housing is torn down, so that the inventory has changed from the previous round.

However, what remains is the concept of the “average” dwelling, and its value has gone up by that 30%. Looking at the city in more detail, however, gives a very different picture.

On June 13, 2016, MPAC gave a presentation to the Government Management Committee outlining the effects on Toronto assessment.

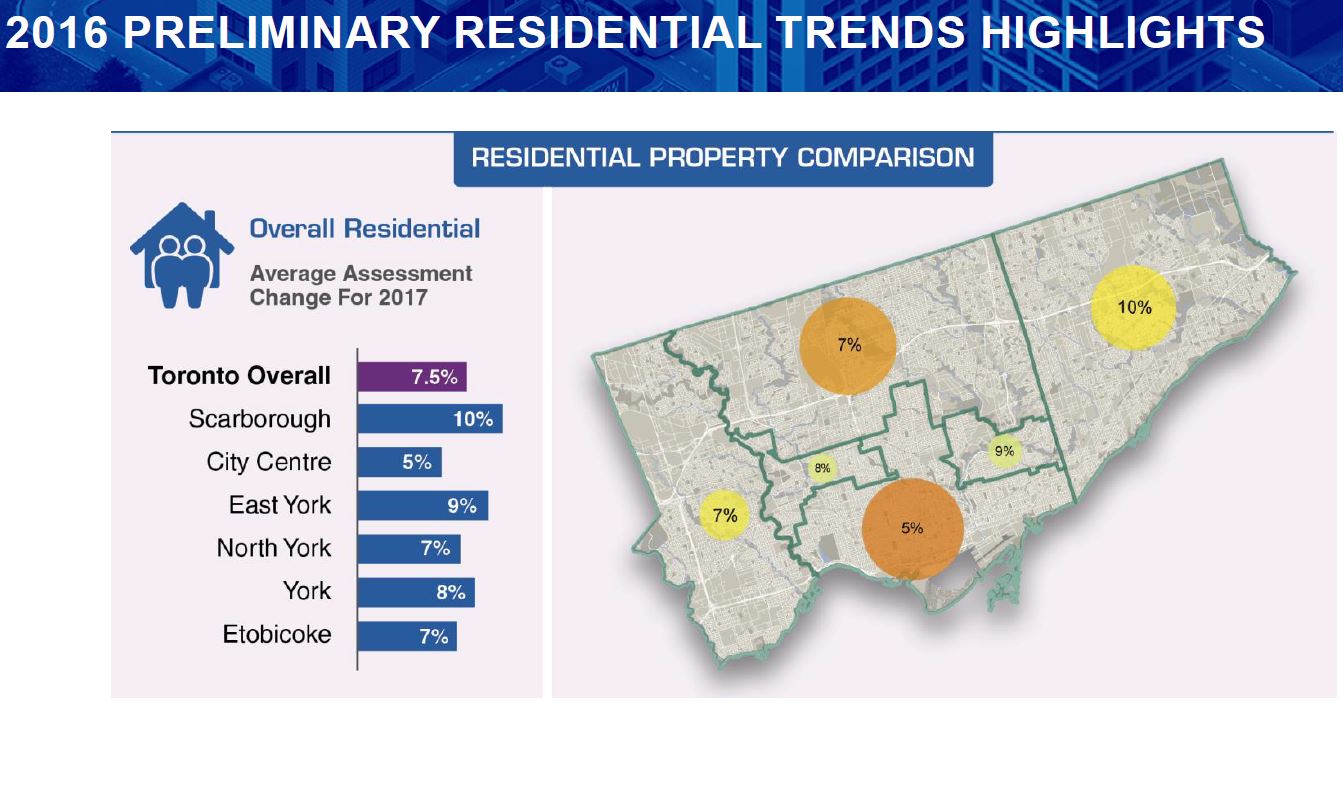

The average increase in property values has been 7.5% in Toronto, but it has been highest in Scarborough and lowest in downtown. This is not to say that values in Scarborough are higher, only that they are growing faster than elsewhere in the city.

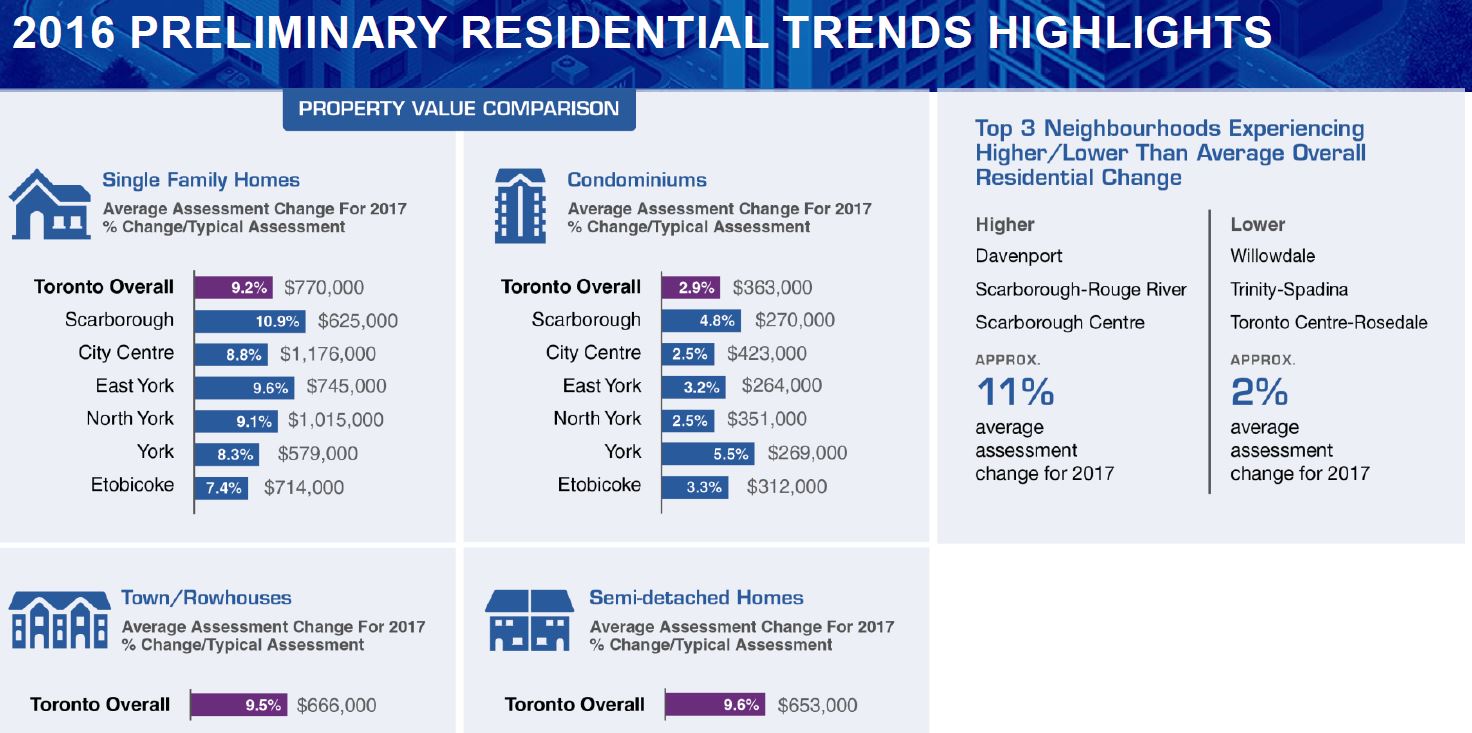

Single family homes rose in value most by percentage in Scarborough, but the average prices there and in York remain lowest in the city overall. Condo values rose much less, notably in areas where the average price is already high (downtown and North York).

When the new assessments are applied for tax purposes, any property whose value went up by more than the average will pay more tax, relatively speaking, and those rising by less than the average will pay a lower tax. (This of course will be offset by any change to the underlying rates and so a substantial drop in value is required to produce an actual reduction in the dollar value of tax paid.)

This shuffling of relative taxes, being revenue neutral, can change an individual property’s tax, but not the city’s overall revenue.

However, MPAC assesses all types of property, and the amount of change will vary from one property class to another. For example, the residential market is strong, and its property values are likely going up faster than for office towers or shopping malls. The result is that the relative share of overall assessment can change between classes. This is independent of any rebalancing processes that might be working through the system.

The new values are implemented (for the most part) on the same four year cycle as MPAC’s work so that one quarter of the change takes effect each year. (Certain properties and circumstances bring a change to the new assessments in one go, or limit the rate at which the change is applied, but most properties go through the four-year implementation cycle.)

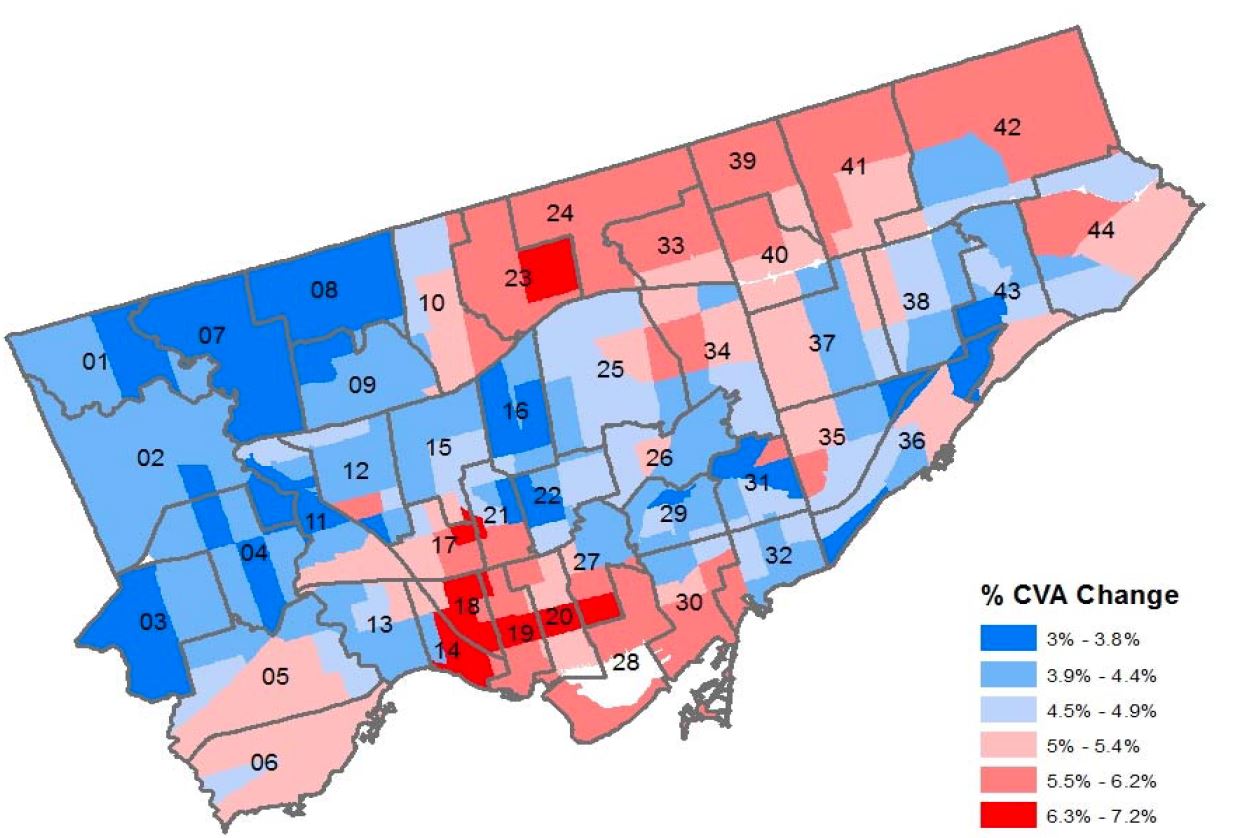

This avoids a major shock to relative taxes in a single year. For the previous cycle, 2012-2016, the process was described in a briefing note and the fourth year’s (2016) effect was shown in this chart:

Again remember that these are percentages, not absolute values of properties. For 2016, there are large differences between portions of the city with some having relatively low rates of increase (but all greater than zero), and some having much higher rates. The appreciation leading up to the 2012 assessments was 23% for residential properties, and the 30% value to 2016 shows how the rate of increase has grown.

A table in the briefing note shows the huge differences in assessed value and number of properties by ward with the lowest assessed value in Ward 8 at $301,320 while the highest is in Ward 25 at $1,375,568. The smallest increase is also in Ward 8 at 3.30% while the highest is in Ward 18 at 6.63%. In other words, property values are lowest in Ward 8 and they were also appreciating at the lowest rate (up to the 2012 assessment). The numbers will be different for 2016, but a detailed map has not yet been published.

Calculating the Tax Bill

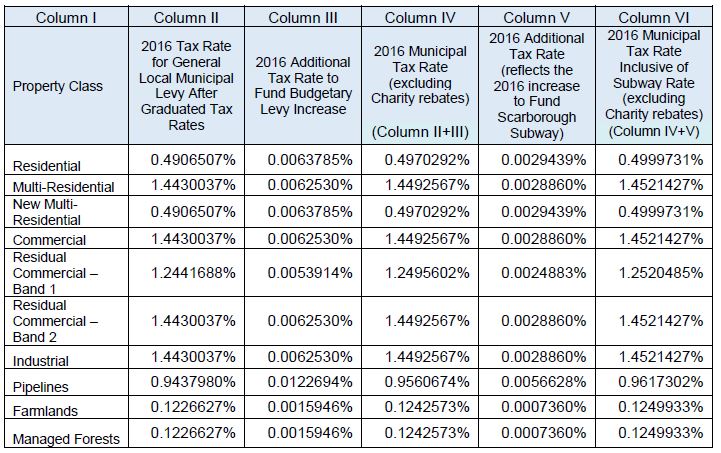

Every year, Council enacts a table of tax rates setting out what will be charged based on the assessed value of properties. For 2016, the rate table looks like this:

For a residential property worth $1 million, the tax to be paid will contain three items.

Municipal Tax $4,970.29 Scarborough Subway 29.44 Education Tax 1,880.00 Total $6,859.73

Notes:

- The subway tax is shown on the tax bills as the ‘Transit Expansion Levy” with no explicit reference to Scarborough, although this is quite clear in the table above. This amount is only the increase for 2016 (0.6%), not the total (1.6%) implemented over the past three years.

- The Education Tax is set by the Province of Ontario, but is collected by the City which has no control over the amount. The rate for 2016 is 0.188%.

- The nominal $1 million value is based on the 2012 assessment which was phased in over the 2013-2016 tax years. Similarly, the new 2016 assessments will be phased in over 2017-2020.

The Scarborough Subway Tax

The Scarborough Subway, as proposed in 2013, was to be funded by contributions from the federal and provincial governments, plus municipal taxes and development charges (DCs). The City’s share would come from $165 million in DCs and $745 million from taxes that would (mainly) finance borrowing. These numbers are based on the originally estimated cost of the so-called 3-stop subway line to Sheppard via McCowan.

The tax increase to fund the subway extension was implemented over three years starting in 2014 with 0.5% in each of the first two years, and a final 0.6% in 2016. The progression is clear in the tax implementation tables below (note that the 2014 table has columns in a different order from those in 2015 and 2016).

The total tax increase, averaged across the city and all property classes has been 4.57% (not including the effects of compounding) over 2014-2016. Of this, 1.6% or slightly more than a third, is the Scarborough Subway tax. This is now “baked in” to the tax rates and revenue from it will continue to flow for three decades. The additional tax collected in 2016 will be about $15.9 million from the 0.6% third step of implementation, and so in round numbers the subway tax will bring in about $42m for 2016. This will inflate along with all other taxes over the lifetime of this levy.

Financing Projects and the Capital Debt Ceiling

Toronto pays for large capital projects through various mechanisms:

- Capital debt

- Development charges

- Capital from current tax revenues

- Contributions from other governments

Another mechanism not included here is a PPP (public-private partnership) scheme. PPPs, in effect, are borrowing from private lenders or leaseback arrangements where a third party builds something and either leases it or operates it on the City’s behalf recouping their investment through annual charges. The effectiveness of PPPs is a separate matter that does not apply to the current discussion about Toronto’s capital financing, although it could become part of the mix in the future.

Contributions from other governments are well understood, although the exact way they arrive may very from project to project (and from one government to another). Some governments prefer to “pay as you play” doling out funds as projects actually need them, while others pay up front as a means of disposing of current surpluses. The latter tactic is used when times are good and unused funds need to be written off into trust funds or reserves, while periods of retrenchment tend to bring less desire to part with a dime until the last possible moment.

“Capital from current” uses tax dollars in the year they are raised to pay for some of the capital construction in place of debt. A rough analogy is a down payment on a major purchase using funds one already has to reduce borrowing and associated interest charges. This amount fluctuates from year to year depending on how much the city feels it can afford. In recent years, the end of some provincial grants triggered a reduction in CFC payments to offset the lost revenue. In effect, the City increased capital borrowing because it lost a source of operating revenue.

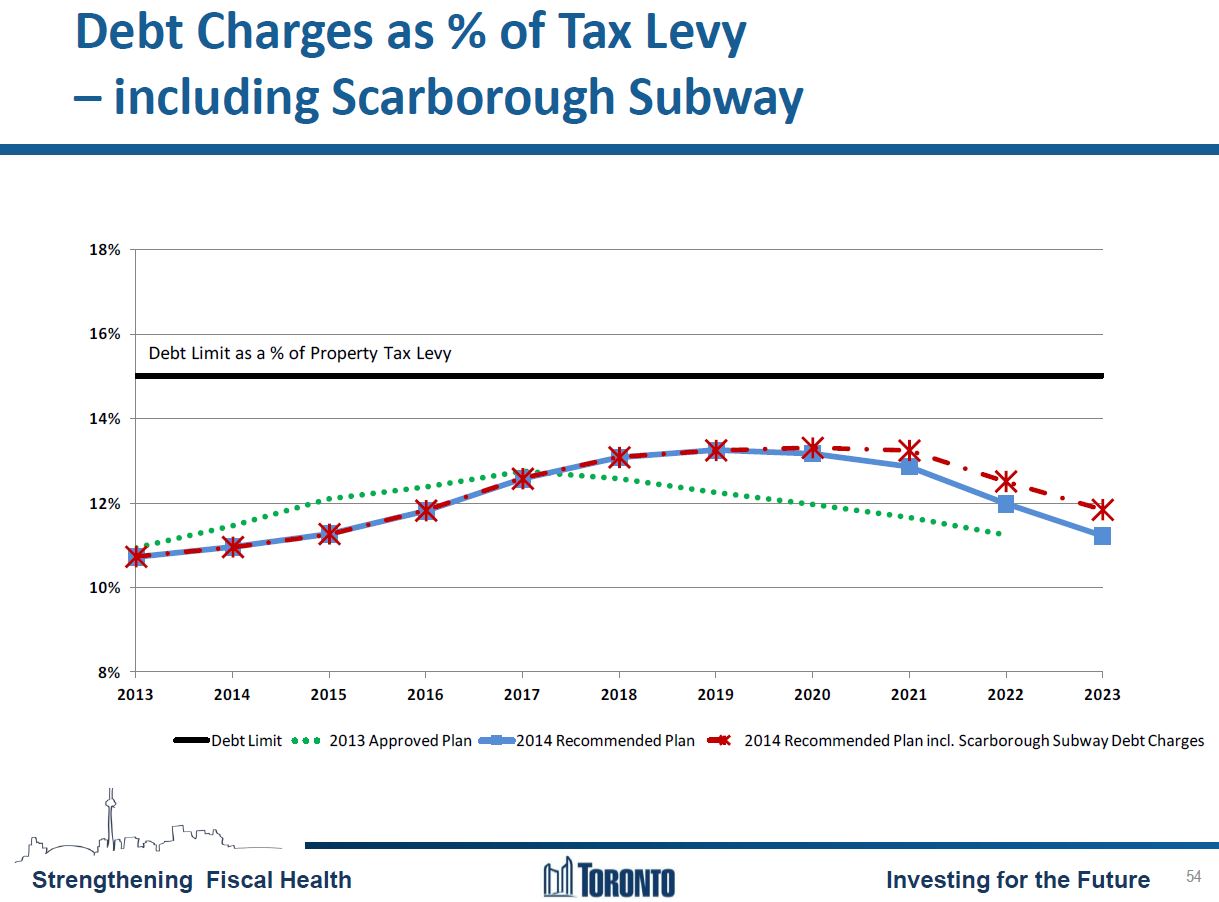

Capital debt is raised to cover spending that will buy something lasting a long time (at least 10 years) and to smooth out the actual payments over the asset’s lifespan. Over the years, the City has accumulated a lot of debt, and to limit its exposure to future economic shocks (not to mention to keep a good credit rating), Council has set an upper limit of 15% for the ratio of annual debt payments to property tax income. There is a Provincial limitation of 25%, but Toronto chooses a lower cap to be fiscally conservative.

This debt ceiling haunts the politicians and the staff at City Hall because the closer Toronto comes to hitting it, the more difficult it becomes to fit new borrowing into the plans. This is complicated by the fact that a project like a new subway line creates a “hump” in the need for borrowing during its major years of construction even though the money to pay off this debt will be collected over a much longer period. The hump drives up the total debt charges in the short term while the City taxpayers are left to digest the debt over a longer period.

While it is attractive to announce major new projects, they have to be paid for, and anything that might happen relatively quickly (e.g. an economic stimulus program) triggers the need for more debt sooner rather than later. The charts below show how the City’s position has evolved recently.

In 2014, the effects of the Scarborough Subway decision in 2013 first appear in the chart. Even without the subway, one can see both the growth in debt charges and a shift in the peak in the curve from 2017 when a downturn was originally expected to 2020. This was caused by the inclusion of more spending in the capital plan, and by a change in the timing of some items to defer their contribution to the peak. However, at this point, even with SSE spending affecting debt levels in the early 2020s (when construction and hence the majority of spending was expected to be underway), the debt level was still under 14%.

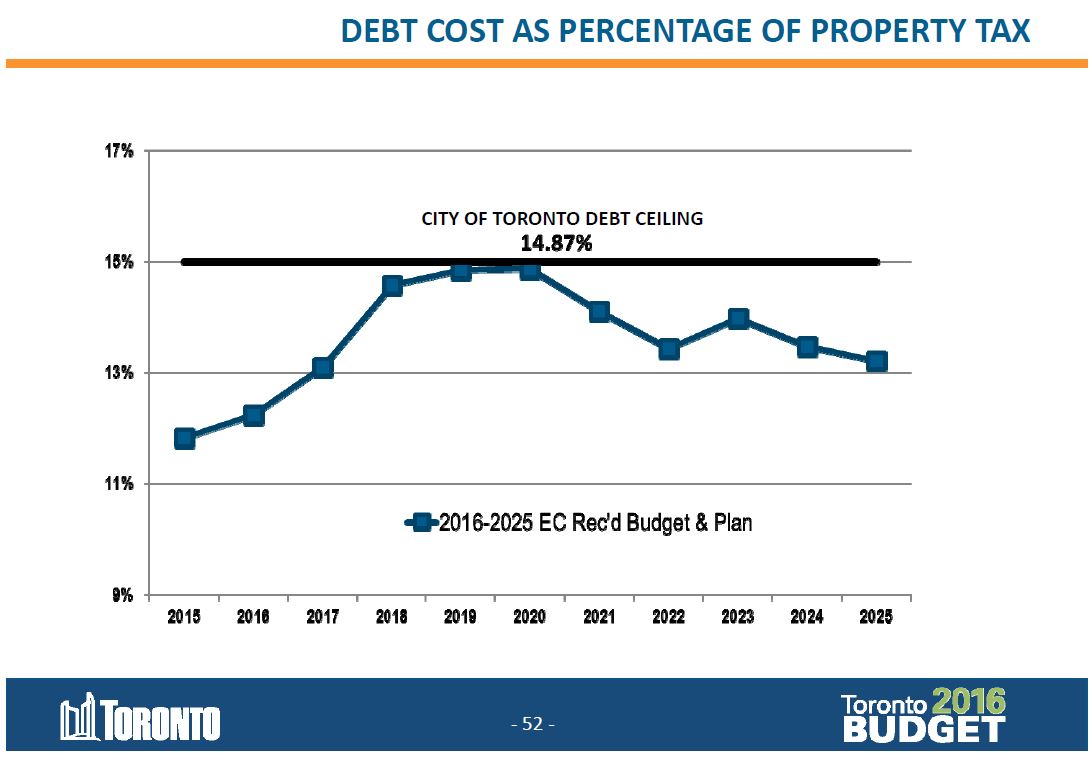

By 2016, however, the situation is quite changed thanks in the main to the Gardiner Expressway project and Council’s embrace of the “Hybrid” option. There is almost no room for new borrowing from 2018 through 2020. The downward trend from 2021 is misleading because many large projects have simply been left “below the line” in budgets, with no funding allocated and hence no associated debt even though many of them are regarded as critical City projects. Some assistance may come from other governments, notably Ottawa, but that is not 100% funding, and the City will have to find its share during a period when there is a desire for high political profile, but no headroom to borrow.

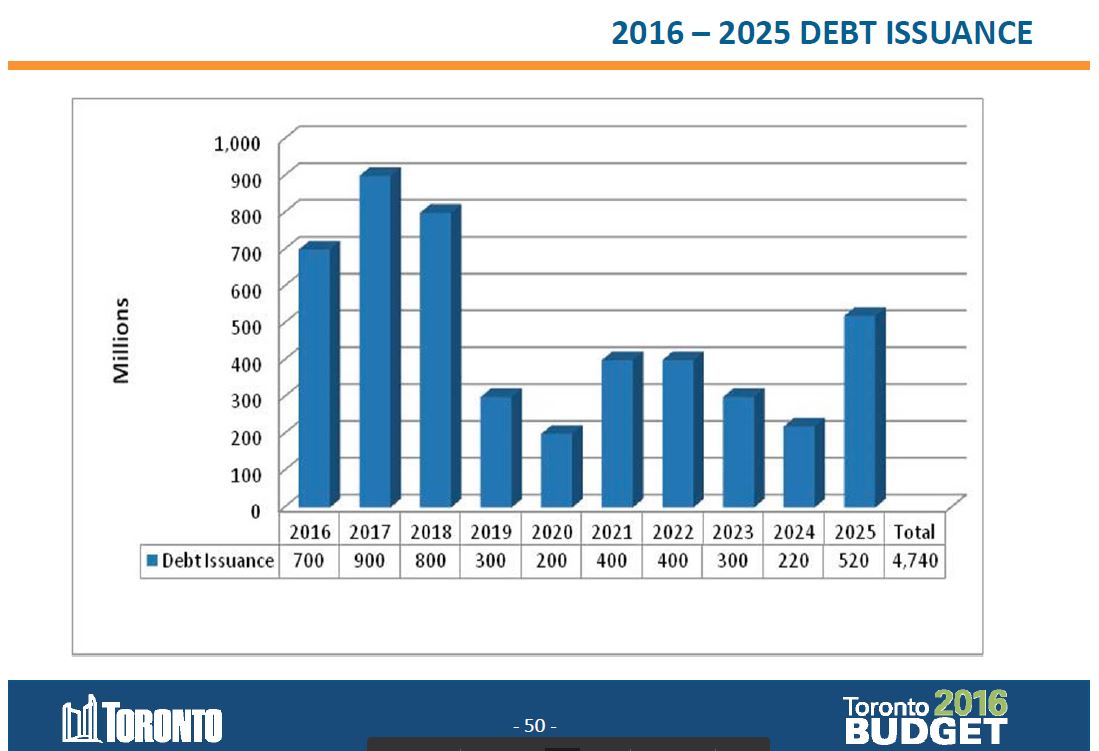

The borrowing problem shows up in a chart of the City’s plans for new debt.

If the City wishes to increase its capital spending, then it must raise new revenues to defray added debt, or to pay for more capital works from current revenues. The amounts of money involved are in billions, and this will not be covered by counting the pencils and paperclips.

Part of the underlying calculations for the debt ratio charts are assumptions about the actual level of future borrowing and of interest rates. The latter affect not just new debt, but the roll over of existing debt. If rates go up, then inexorably so will interest costs as renewal of existing debt comes due.

Note that the Land Transfer Tax, from which Toronto substantially benefits, is not included in the debt ceiling calculation because it is not part of the “property tax”. LTT growth has been strong, but if the Toronto real estate market weakens, this revenue cannot be counted on for the same time period as debt that is issued based on long-running, stable revenue from property taxes.

We have reached a point where new projects cannot simply be approved without a serious discussion of how the City will pay for them. There are grand plans, but there isn’t even enough money to pay for necessary capital repair budgets such as at the TTC or Toronto Housing. New projects will require new money, and lots of it.

Mayor Tory proposes a City Building tax that would begin to operate in 2017 and would roughly parallel the Scarborough Subway tax. However, the amount of capital it can finance at the rate proposed is limited. Whether taxpayers have the stomach for higher taxation is hard to say.

One might argue that the subway tax both showed the way to a future regime, but could also have “poisoned the well” by showing how major projects can push up taxes. The problem is compounded by the effect of rebalancing which loads the primary burden for any new taxes on residential property.

Tax Increment Financing

In a previous article, I wrote about the scheme advanced by SmartTrack supporters to use incremental tax revenue presumed to arise from rapid transit construction as a source of funding. Leaving aside the absence of enabling provincial legislation, TIF supporters make several fundamental blunders in their analysis:

- Assignment of specific elements of the tax stream to the construction of specific projects is a challenging task involving assumptions about what might or might not occur in the future. Some development will take place in the absence of transit spending because there are many other incentives including the inherent attractiveness of a site, or because other transportation links provide the needed capacity (GO vs the TTC downtown, 401/DVP vs Sheppard subway in North York).

- Multiple projects could have a claim to the taxes due from a new development. For example, the Great Gulf Unilever site will benefit from (and may be encouraged by) the provincial GO/RER plan as much as by SmartTrack or the Relief Subway both of which could serve the site.

- Some development will occur well in advance of new transit construction and can only be thought of as “due to” a new line in a remote way. Liberty Village, for example, has developed with little more than a few, now overloaded, streetcar lines.

- The authors presume that added tax revenue from the “uplift” of property values can be assigned to the TIF revenue stream, even though this concept has no legislative definition, and the CVA process explicitly depends on a revenue-neutral approach to the effects of rising values.

- The authors further expect to have access to the provincial education tax stream even though new development brings added costs to the school system.

It is possible that some tax revenue may legitimately be the direct result of new development triggered by transit spending, but this is not on the scale foreseen by TIF advocates. Moreover, the whole matter of additional infrastructure and social costs brought by development must be considered, not simply the construction cost and financing of one rapid transit line.

Misapplication of TIF could leave taxpayers on the hook for costs that might have been borne from general taxes on new development. With that revenue diverted to pay for a specific capital project, the remainder of new City costs would fall to everyone else. TIF may be a workable source of revenue, but the dishonesty with which it has been presented should warn us all to be wary of its actual value.

In Conclusion

The end of this long story should be no surprise. The City Manager warned recently that the current spending patterns are not sustainable for either operating or capital budgets. Council is averse to finding new revenues, especially those that would generate substantial income. It is content to contemplate only small-scale changes, tweaks of its own budget and minuscule taxes that would annoy almost nobody, but bring almost no revenue. There is no sense that most Councillors up to and including the Mayor are capable of dealing with the City’s acute financial situation beyond recommending a dose of “efficiency measures” to avoid inevitable decisions.

A proposal to tax commercial parking spaces brought howls from the business community who have been getting a free ride on the rising cost of City services.

Residential property taxpayers (who in turn are a goodly share of actual voters) might be congratulated for shouldering the majority of the tax increases of past years in the name of making Toronto more attractive to business. That process will continue for four more years during which residential tax rates will go up at least 10% while non-residential rates are static or even fall.

New transit project financing for the City’s share will land disproportionately on residential properties unless it is implemented in a post-balancing world where all property classes bear an equal share of the increase, or unless major new sources of revenue beyond property tax pay the bills.

The City has a backlog, a wish list, of capital projects that total $29 billion for which there is no funding today. Some of this might benefit from newfound generosity in Ottawa, and even Queen’s Park may someday come in as a partner. However, none of this will happen without the City pulling its weight, and that means finding new revenue. Whoever is asked to pay will scream, and their complaints, the chorus of “no new taxes”, will inevitably become fodder for election campaigns to our detriment.

Notice that the tax rate for multi-residential buildings (apartments) is 3 times that of residential properties. Barbara Hall, to her credit, promised to end this injustice in her failed bid at reelection as mayor. No one else seems to care.

Steve: It will only go down to 2.5 and stop there. The real problem is that residential buildings should be in a different property class so that tenants get the same treatment as homeowners. As things now stand, roughly 1/3 of rent paid by tenants goes to property taxes.

Note that such a change will also require provincial buy-in because they set the education portion of the rates.

LikeLike

I was not aware (or had forgotten) about the “leveling” of the tax rates. For anyone keeping score at home, this appears to have been done in “Bill 53, Stronger City of Toronto for a Stronger Ontario Act, 2006”.

Specifically in Part XI: Traditional Municipal Taxes (pp 273-287). So much for subsidiarity.

(Note also there is/was John Fraser’s ‘Bill 53’ from 2015, Protecting Passenger Safety Act, that is still in committee.)

LikeLike

You have written the clearest explanation of Toronto’s tax dilemma that I have ever seen. I think that the issue has been confused in recent years by articles in the local press that purport to explain how unfair the system is to everyone but the fat cats.

Barbara Hall was the prototype for the present Kathleen Administration; accomplishing, or attempting to accomplish a great deal of necessary reform and rebuilding that was often too low key or complex to be appreciated by the voting public; especially the people who relied upon the press for their information.

For those of you who are upset over the present 416/905 inequalities; I can tell you that it was once much worse. Circa 1960, Leaside’s residential mill rate was about 28, and the old City of Toronto’s about 45.

Steve: Just for completeness, back in the 1960s, the assessments were all over the map too, and so a direct comparison of mill rates does not necessarily tell the whole story.

LikeLike

The lack of equality varied from city to town to township. I moved from North Toronto to Leaside in 1948. With its huge industrial assessment [C 50%], Leaside was a taxpayers’ paradise. The relatively undeveloped townships [eg North York] had difficulty providing basic services during the sudden rash of new housing developments immediately after WW2.

LikeLike

Subways should be built using HST and operated using property taxes and fare free transit to encourage transit use thus reducing pollution, road fatalities, etc.

LikeLike

This is so embarrassing, the whole subway fiasco. I feel like I have been hearing the same argument in circles for 10 years.

LikeLike