Updated December 1, 2017 at 11:15 am:

The preliminary City of Toronto operating and capital budgets were presented at Toronto’s Budget Committee on November 30, 2017.

Operating Budget

To no great surprise for seasoned budget watchers, the Two Hour Transfer was not included in the funded budget, but instead appears among a long list of unfunded new or enhanced services. The total value of these proposals is $41.3 million (after considering any associated revenue), and they are competing for a much smaller amount of available headroom in the operating budget. (The list is on pp 12-14 in the appendices linked above.)

Although Council may approve many wonderful initiatives and the Mayor may hold many press conferences and photo ops exulting in the decisions, the money to pay for them is often not part of Council’s decision. What actually happens is that these are “nice to haves” thrown into the coming year’s budget hopper on the off chance funding will materialize by budget time. This has the effect of throttling the will of Council and feeding all of its decisions through the much more conservative outlook of the Budget and Executive Committees.

Council further limits this process by passing a budget directive early in the cycle (usually late spring) directing that property taxes for the coming year not rise by more than the rate of inflation. The actual increase is below inflation because commercial property rates are on a long downward trend thanks to rules imposed by Mike Harris to rebalance the relative tax levels for commercial and residential properties in Toronto. This will not complete until, probably, the 2021 budget after which tax increases will apply equally across the board.

Of the new revenues Toronto will receive in 2018, property taxes are actually only a small component, but Council debates inevitably turn on this source as a benchmark. The actual tax increase anyone sees is the result of several factors:

- the tax rate change for their property class;

- changes, if any, in separate levies such as the Scarborough Subway tax and the Mayor’s Infrastructure tax;

- updated and/or phased in changes to the assessed value of property;

- policy directions such as rebalancing rates between property classes (e.g. commercial vs residential).

Other new revenues can flow to the City through various rate structures notably TTC fares, although these have been frozen for 2018. A small increase in fare revenue is expected compared to the 2017 budget thanks to a changes in the relative number of fares paid of each type (passes, tokens, cash).

As things stand today, the funding to pay for the Two Hour Transfer simply isn’t there, but it may be found, almost like magic, as the budget process unfolds from now through February 2018 at Council. Another transit fare proposal, the first phase of the “Fair Fare” scheme in the Poverty Reduction Strategy, is also not funded.

This process creates a drag on implementation of new programs unless there is strong political support from the Mayor and his voting block on Council, and should serve as a warning to advocates for schemes such as the Ridership Growth Strategy. With luck, there will be proposals before the TTC Board before the hiatus of meetings for the 2018 elections, but anything the Board approves will be considered as an “enhancement” going into 2019 and could well be derailed. Add to this the chronic problems of vehicle and garage space shortages at the TTC, and there is a recipe for seeing little real growth in service until at least the 2020 budget year if not later.

This is the combined effect of a process that has valued capping spending above all other goals for many years. Infrastructure that would be needed to support growth doesn’t exist and has a multi-year lead time, and even the vehicles the TTC owns run less service than they could because improving service never comes with enough revenue to cover costs.

Passengers who have shorter waits or are less crowded do not represent extra revenue, and the marginal gain lies only with new fare-paying trips attracted to the TTC. On a grand scale this is seen for 2018 with the Vaughan subway extension where net new revenue does not come close to paying for the added operating cost of service, but this happens at a smaller scale whenever a bus runs more often and less crowded, but mainly with passengers who were already on the system.

A further problem for constrained budgets is that the cost of existing service goes up through inflationary pressure, and the population requiring municipal services including transit continues to grow. City management use that growth to show how the tax burden is actually declining on a per capita basis from $4,480 in 2010 to $4,262 in 2018 (presentation, p 17), and this is considered to be virtuous when in fact it shows not just “efficiency” but also a decline in service provided. The effect on individuals varies depending on which municipal services they consume, and the program-by-program effect is never reported.

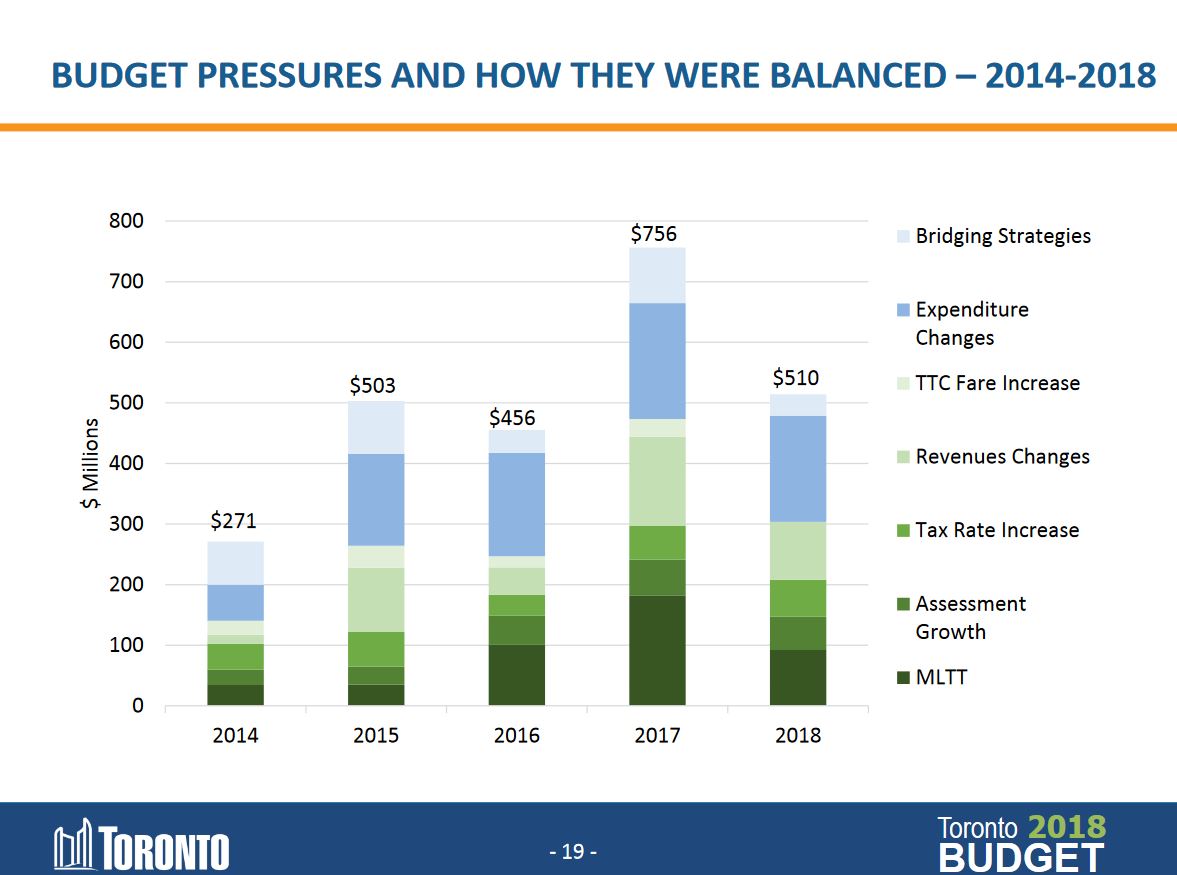

Every year, the budget is hauled into balance through a combination of new revenues, reduced expenditures and “bridging”, a term for various accounting “fixes” that get the City past short-term problems. (Apologies for the subtlety of the colour changes in the chart below. It is from the City presentation.) Note that the values below are “deltas”, the change from year to year, not the total revenue or spending in each category. Expenditure cuts (darker blue) have been a large chunk of the savings in recent years. By comparison, TTC fare increases are small change within the larger City context and, of course, there is no increase in 2018, a policy direction endorsed during the 2017 budget cycle.

However, City budgets are debated at the margin in that any fine tuning is achieved by tweaking revenue sources to accommodate new spending, and the proportional effect on thinks like fares, property taxes and other user fees tends to be higher than for the budget as a whole. The reason for this is that much of the City’s revenue comes from sources that Council cannot “tweak” in the course of setting its budget, and so the effect on what remains is higher.

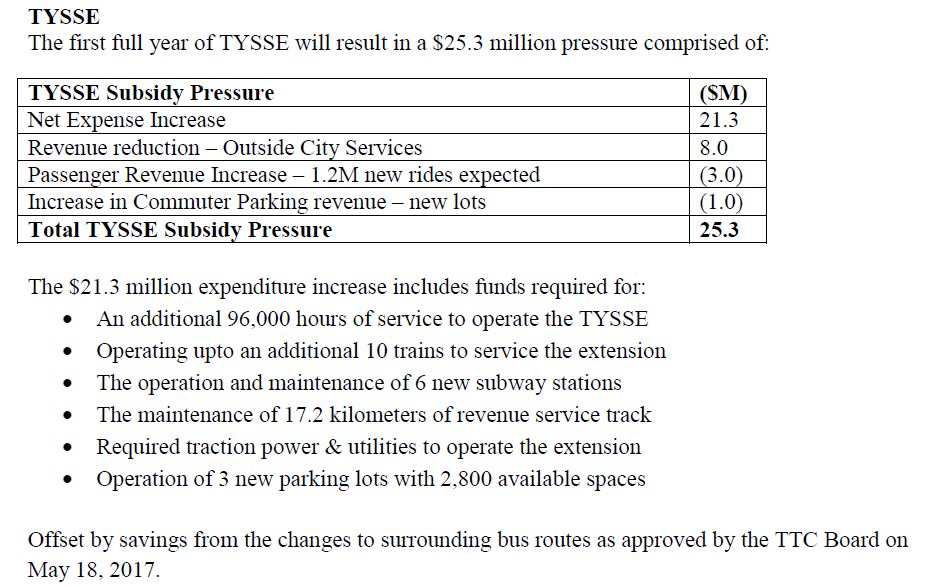

The TTC Board decided that it would include the money sitting in the Transit Stabilization Reserve as 2018 revenue, just as they did in 2017 (although in fact this was not needed because of better-than-budget results). This keeps the year-to-year subsidy increase down to $24 million paying mainly for the new cost of the TYSSE and for transitional increases in fare handling while Presto and the legacy fares both remain in place. Using that reserve is an example of a “bridging strategy” because the reserve will not be available in 2019 if it is depleted in 2018, and new revenue will be needed to replace it. That $24 million pressure from the TTC (with more to come from unfunded proposals) crowds other City departments and agencies by taking the lion’s share of new spending.

Among the factors listed in the revenue and expenditure changes for 2018 (p 27), there is a section headed “Prior Year Decisions”. This includes the TYSSE effect, but does not include the cost of the fare freeze decision on the 2018 revenues. Had there been a fare increase, politicians would be forced to explain to riders how opening a new subway is not free and how York Region gets a free ride on Toronto taxpayers.

The City’s overall revenue and expense budget is summarized in the chart below. The TTC’s total expenditures of $1.974 billion consume about 18% of the budget, but 63% of this is paid for through the farebox. (Note that there is a common problem when “farebox” recoveries are cited for the TTC because other revenues such as advertising and parking are sometimes erroneously included as if they were rider contributions. Also, occasionally, the TTC funds some capital costs from current revenues and these do not properly belong in the “operating cost recovery” calculation.)

When the available revenue including assessment growth and inflation in property taxes are considered, the City has a small surplus of $3.4 million in the preliminary budget. A further $5 million will be available from a pending change in taxation of vacant property, although Council has already directed that this go toward the Poverty Reduction Strategy. Without further adjustments, these are the only funds now available to pay for the $41 million in approved but unfunded initiatives including the Two Hour Transfer.

Capital Budget

On the Capital side, there are a few points worth noting in the City Budget that bear on the TTC’s funding.

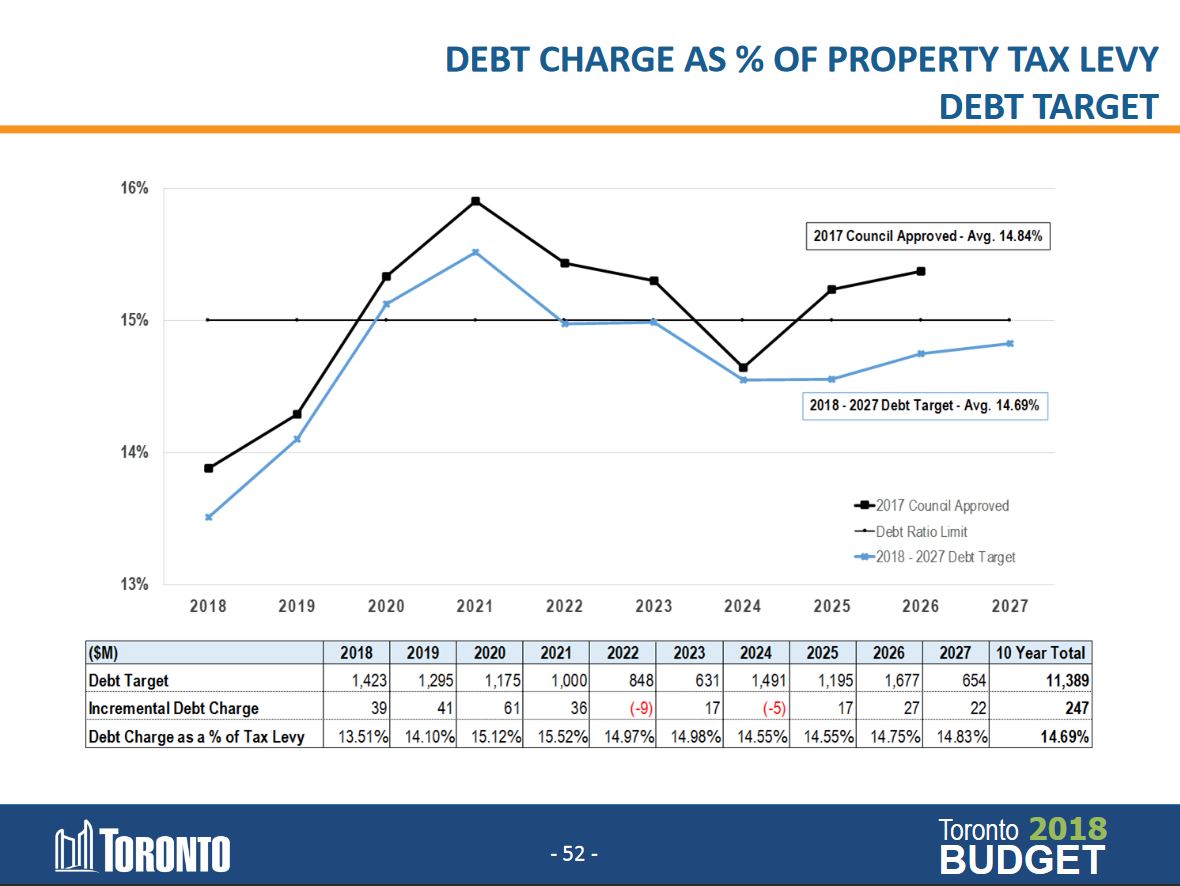

The City of Toronto has a policy that total debt service payments should not exceed 15% of property taxes. This was changed in recent years from a hard cap to one that considered the 10-year average debt ratio mainly to deal with a bulge in borrowing that will peak in 2021. That bulge would affect projections well into the next decade as lower-than-average borrowing in 2018-19 slips off of the chart but must be replaced by comparably low numbers in 2028 and beyond to hold down the average while the 2021 peak is “digested”.

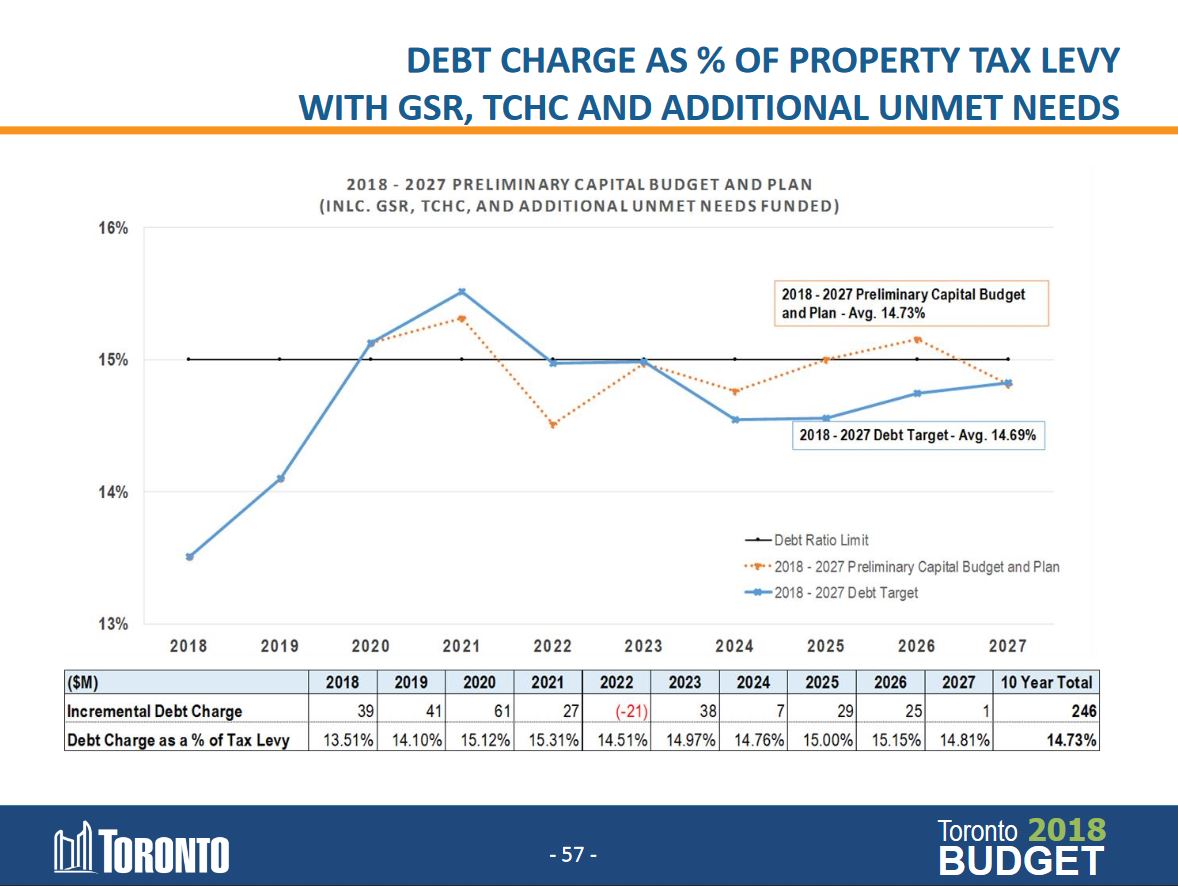

Various adjustments to the budget change the shape of this chart and somewhat tame the peak. There are additions (funding for TCHC repairs and other unspecified “unmet needs”), but new provincial gas tax revenue announced in 2017 allows a reduction in the debt load producing the revised chart below.

The debt limitation, together with limited provincial and federal funding, is directly responsible for the TTC’s enormous list of unfunded projects. The new gas tax revenue will generally not go to transit projects (except possibly under “unmet needs”), but will offset other City borrowing needs.

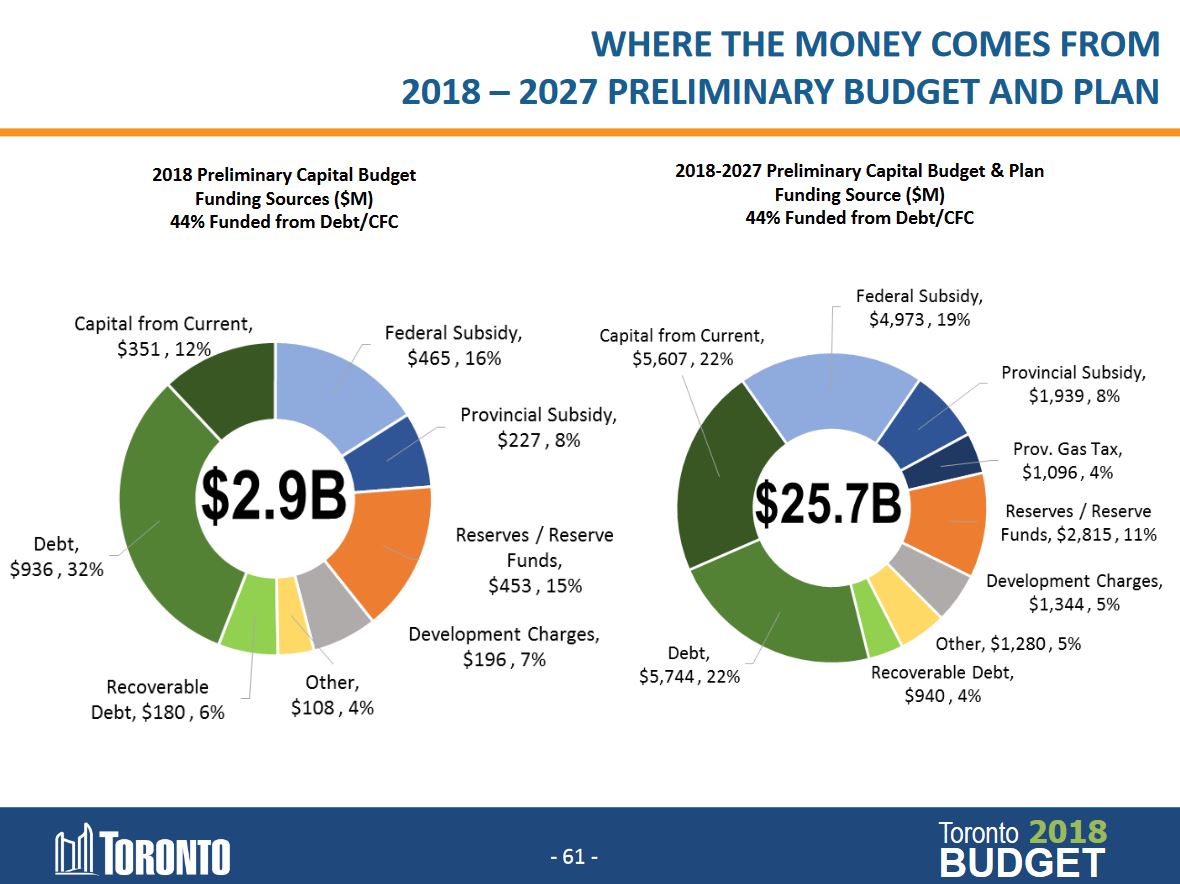

Another change in projected City financing will be an increase in the “Capital from Current” amount. The proportion of funding provided by this source will rise from 12% of the 2018 budget to 22% in the ten year plan while debt falls from 32% to 22%. This will shift more of the spending in later years of the plan into the operating budget, although the dollar increase may be offset by a reduction in total annual funding needs assuming no major projects are added without dedicated revenue sources and/or subsidies from other governments.

Even with all of this spending, the “state of good repair” backlog across the city will continue to grow, notably at the TTC. This plan understates future funding requirements by its failure to include the TTC’s SOGR projects that are known to exist, but not included in the City’s plans. (Some other City departments, notably Transportation and Facilities Management, also have large unfunded repair backlogs. See p 63 of the presentation.)

Updated December 1, 2017 at 9:15 am:

The budget presentations, which contain slightly different information from the budget reports, are now online.

The Capital presentation has a more detailed breakdown of the “Capacity to Spend” reduction, and I have added this, plus a few comments, to that section of the main article (scroll down to the end).