Ever since Mayor Tory’s election campaign, we have been told that SmartTrack is a something-for-nothing project that would bring vastly improved transit service to Toronto at little or new added cost to taxpayers. This would occur through the hocus-pocus of Tax Increment Financing TIF).

For those new to the subject, the premise here is that building a new transit line causes property values to rise and new development that would not occur in the absence of the transit investment. That generates new tax revenue that could be used to pay off the construction debt. However, the city’s staff, who are bending over backwards to make Tory’s transit plans workable, do not see TIF as coming close to paying for Toronto’s share of SmartTrack.

See also:

- Jennifer Pagliaro’s article in the Toronto Star, “Major unknowns, risks in funding Tory’s SmartTrack plan remain ahead of vote”

- Tricia Wood’s article on the Torontoist site, “Crunching the Numbers on SmartTrack’s Ridership”

- Sean Marshall’s article on the Torontoist site, “Here’s What the Development Opportunities at SmartTrack Stations Look Like”

The election premise was that SmartTrack would be built at a cost of $8 billion, would provide a total of 22 stations and frequent service over a route from Markham to the Airport Corporate Centre (south of Pearson Airport). This would be shared equally by all three levels of government making Toronto’s share about $2.7 billion, if one believes the premise of the campaign.

The situation has changed over the past two years. The Eglinton branch of SmartTrack as a railway operation was never a good idea, and it has reverted to the original LRT proposal from Transit City. Tory takes advantage of the more closely-spaced stops on the LRT to bolster his SmartTrack station count. In fact there would be more new LRT stations than SmartTrack/GO stations as the plan now stands.

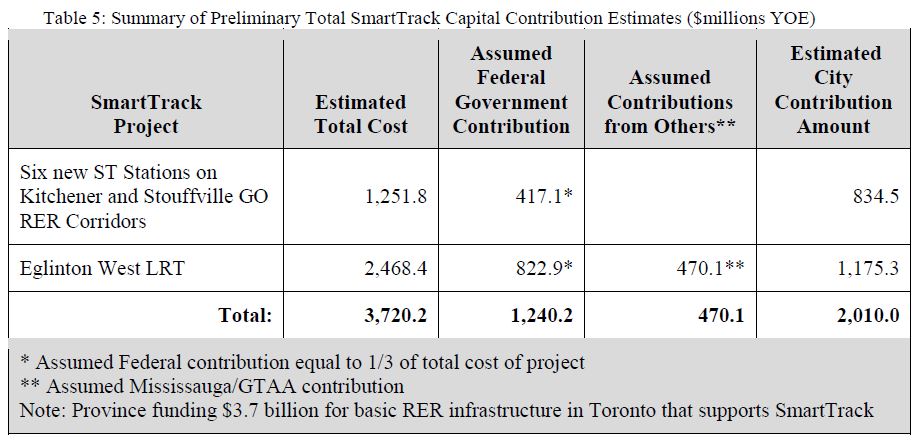

GO Transit’s Regional Express Rail (RER) program will see widespread infrastructure and service improvements beyond which SmartTrack will only add six new stations. The projected cost of “SmartTrack” has gone down, but the City’s share remains above $2 billion. (The values below do not include cost of financing and risk transfer under Ontario’s procurement system that could bump these numbers by 20%.)

[Source: Transit Network Plan Update and Financial Strategy, p. 11.]

City staff argue that the benefits available from “value uplift” of existing properties will be low, and they have not included this in their calculations. From new development, the added tax revenue would be $857.1 million over the life of the financing scheme, and to be conservative, staff recommend that only half of this be presumed for SmartTrack financing.

This calculation does not address how the services new commercial or residential development will require would be financed if some or all of their new tax revenues were dedicated to SmartTrack.

The chart below shows the considerable spread between TIF and Development Charges (DCs) revenues and the actual requirements for SmartTrack financing, including the LRT line on Eglinton from Mount Dennis to Renforth.

[Source: Transit Network Plan Update and Financial Strategy, p. 12]

The two percent tax increase would be applied to residential property with only a .67% increase for commercial property. This arises from the City’s policy of rebalancing residential and commercial tax rates, a process that will complete in 2020. Given the timing of borrowing for SmartTrack, one must ask whether the balancing policy should apply in this case, and whether it is time for the commercial sector to pay its full share of taxes that will be collected almost entirely beyond the date when the balancing program completes. (Note that “commercial” includes rental apartment buildings.)

The estimates for TIF and DC revenue arise from projections in a report, Commercial & Multi-Residential Forecasts for the Review of SmartTrack, by Strategic Regional Research Alliance (SRRA) that was commissioned by Council to examine the question in detail. (The SRRA report begins at page 8 of the document.)

To put this in context, SRRA was co-founded by Iain Dobson who was an advisor to Tory’s election campaign. In May 2014, just as the SmartTrack campaign started, he was appointed to the Metrolinx Board during Glen Murray’s final days as Minister of Transportation. The consulting contract was awarded by Council on a sole source basis.

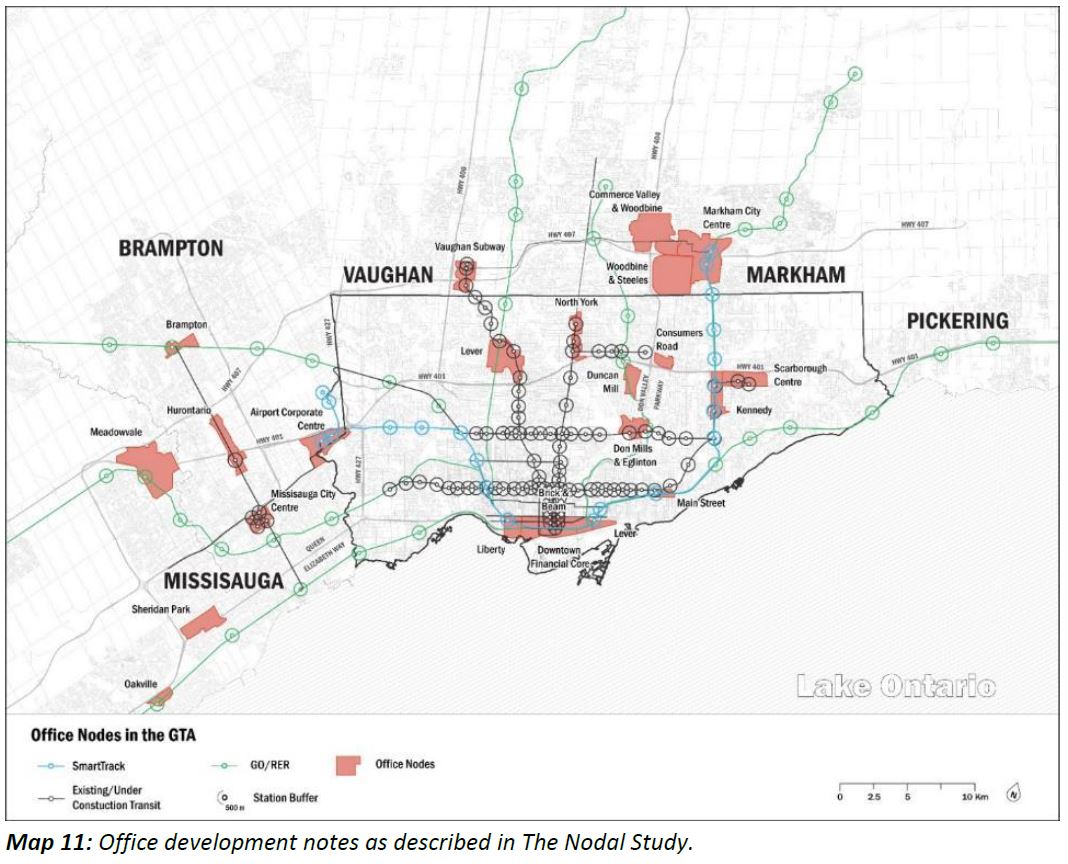

When SmartTrack was proposed, the intent was to improve access to areas of potential development. The following map shows these areas and their relationship to the SmartTrack corridor.

[Source: SRRA study at p. 21. “Nodes” is misspelled in the map title, and the Downsview node is mistakenly labelled “Lever”. How this might reflect on the care taken on the report I leave to the reader’s judgement.]

Several of the nodes lie outside of Toronto or far from the SmartTrack corridor (blue line and circles). These will either not produce new tax revenue within the 416 or they are too far from ST to benefit from its construction.

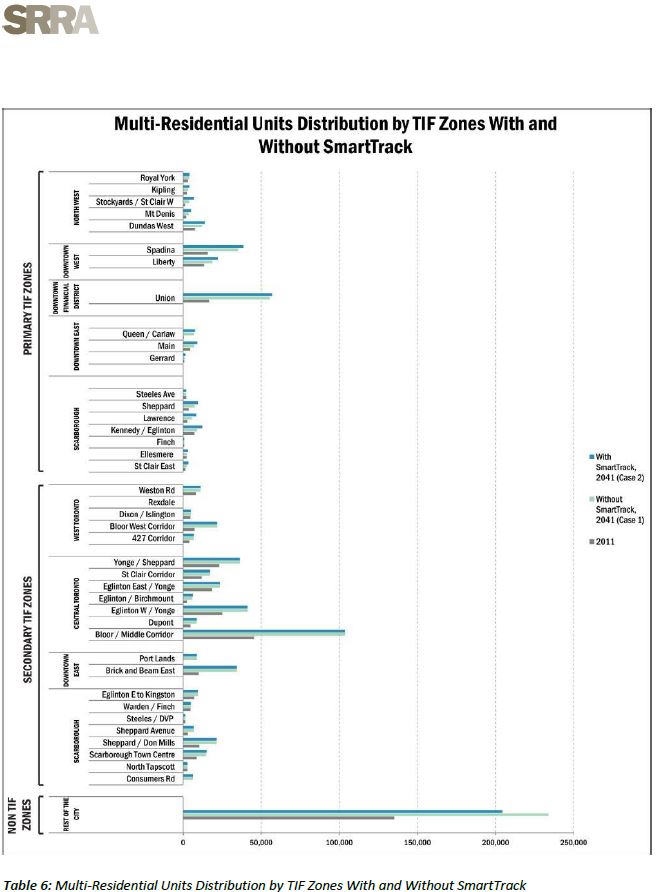

A vital question, then, is whether the amount of development contemplated in the January 2016 SRRA report and resulting tax revenues will actually flow to the city. SRRA’s analysis begins with a map of the “TIF Zones”, the areas around stations where tax increases could be expected.

Many of the stations are existing or planned GO stops that will see added service without any SmartTrack investment, and ST adds nothing to them (Milliken, Agincourt, Kennedy, Main, Union, Bloor, Mount Dennis). The map also shows a station at Spadina that will not be part of the upgrades planned for the ST corridor.

Although many zones are shown, most of them will not be affected by SmartTrack as it is now proposed, merely the addition of six stations to the GO Transit map: Finch East, Lawrence East, Gerrard, East Harbour (Lever), Liberty Village and St. Clair.

Although the SRRA report discusses the methodology for analysis of the effect of SmartTrack in the TIF zones, it does not provide a dollar value for the actual tax increments this would produce, nor a description of how this might be calculated. Numbers cited in the City report imply that a more detailed breakdown exists for the SRRA data, but that it has not been published.

An important component of the stimulus attributed to SmartTrack is the construction of additional residential units because ST would make jobs in the outlying centres (notably Markham and the airport) easier to reach and thereby allow reverse commuting. However, there is no “ST service” per se, only the provision of stops where riders might board GO RER trains running less frequently than original claims for ST itself.

Projections for employment and residential growth are shown in charts.

The core area remains the primary location for employment growth, although the projection with SmartTrack diverts some of this to other areas, notably the Queen/Carlaw area (i.e. the Lever site) and Liberty Village. The latter is a bit of a stretch because the station would be located at the northeast end of the district while commercial development, such as there may be, will be toward the southwest.

An important distinction here is that in the “secondary zones” (those along transit corridors other than ST) and in the non-TIF part of the city, the projected employment with ST is generally lower than if ST exists. In other words, potential development that might hold these employees shifts into areas where it contributes to projected TIF revenue.

A similar situation applies with residential units.

The city adjusts for this numerically in their backgrounder on City Funding and Financing Strategy.

What is not clear, however, is which of the TIF zones are included for this analysis, in particular those which are at existing GO stops, nor whether the effect of ST’s having no marginal service beyond that provided by GO RER has been take into account. If all zones were included, has the potential revenue due only to SmartTrack been overstated?

A similar problem exists for the calculation of Development Charges because the formula for these, set by provincial law, makes them applicable only to the benefits provided by the expenses undertaken by the City, not to improvements others such as GO might provide nor to improvements existing transit riders might obtain from the new stations/services. This considerably limits the scope for recapture of costs through DCs. (In Scarborough there was was a successful appeal by developers that reduced DCs attributable to the Scarborough Subway. This was based on a higher estimate used for new riders in the DC calculation, and hence the proportion of riders from new development, than in a later estimate.)

There is a more general problem with DCs in that they affect every new building in the city, not just those along the transit corridors. Developers who do not benefit from the projects these charges help to finance are not enthusiastic about building yet more costs into the base borne by would-be purchasers.

Questions for the City

All of this raises many questions about the validity of the calculated TIF revenues available to finance the SmartTrack scheme. I have sent queries about this to City staff, and await a reply. This article will be updated when more information is available.

Council will debate the SmartTrack reports at its meeting beginning on November 8, 2016. Here, in brief, are my questions.

- The staff presentation to Council expresses commercial growth in thousands of square feet while SRRA uses employment. These can be converted to each other with a ratio, but what number has been used? How do the City numbers relate to the SRRA values?

- The bar graphs in SRRA’s report do not include actual values making direct calculations such as selective inclusion or exclusion of TIF zones difficult. What are the numbers?

- Which TIF zones were used for the calculations in the City presentation? Only the six the City is paying for, or zones at all “SmartTrack” stations even though many of these are GO RER locations to which ST will not add any service?

- What adjustments in projections have occurred between the original SRRA estimates and those used in current City estimates?

- As with TIF, have DCs been calculated only based on the six added “City” stations, or for all of the ST/RER locations?

- TIF revenue is projected to grow uniformly and across all included zones. Is this a realistic assumption, how much growth is projected in each zone, and when is this expected to occur?

- If the SmartTrack tax were implemented at the same rate across all property classes, at what level would the tax be set?