Rummaging in financial reports can lead to interesting discoveries, although we usually read about them when some financial hound exposes dubious accounting practices and drives down the value of a company’s shares. Indeed, the Globe’s David Milstead had a long article on just how pervasive the use of non-standard accounting has become in corporate reports.

In the public sector, various mechanisms are used to reduce apparent debt and exposure to future costs. Some of these involve judgements about just when bills and revenue will roll through the door, or of exactly who will pay these bills as they come due.

In a previous article, I wrote about the TTC’s newfound mechanism called “Capacity to Spend” which reduces future funding requirements by roughly as follows:

- Project estimates show that the TTC will need about $9 billion to fund its “Base Capital Program” over the next ten years. This does not include special projects such as subway extensions, nor does it include a long list of “below the line” projects that have not yet matured to “approved but unfunded” status.

- Yearly capital spending by the TTC is typically lower than the budgeted value, but the main reason is that work took longer than expected, or projects were rescheduled into future years. Only a few of the underspent accounts arise from actual savings thanks to lower than expected costs or project cancellations.

- Nonetheless, the TTC has decided that its real funding requirement for 2017-2026 is now almost a billion lower than has been claimed for many years running.

This is a basic case of revaluing the exposure to future costs to make long term funding (including borrowing) needs appear lower than they really are. This year brings an extra incentive with federal funding that requires matching municipal contributions, money Toronto does not have. But hey, presto!, if we reduce the future spending, at least on paper, we have “found” money with which to pay the local share of the fed’s new program.

Meanwhile up the road at Queen’s Park, a lovely myth for the past near-decade is that there is a “municipal share” to the GO Transit capital program. Most people don’t know about this, and Toronto has refused to actually pay into that pot for several years.

The mechanism was set up back when GO Transit was a separate agency, and it has been passed down through successor organizations to its current home, Metrolinx. The amount of money outstanding is not trivial.

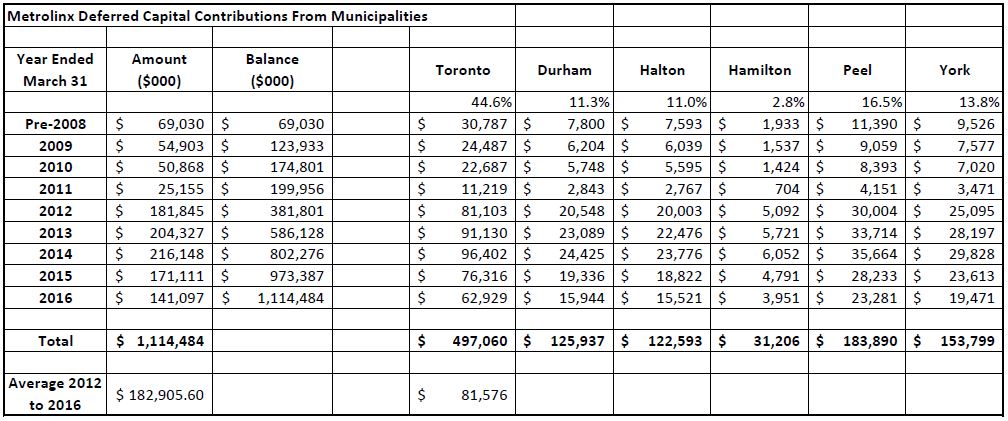

By the end of Metrolinx’ fiscal year March 31, 2016, the accumulated balance of deferred municipal contributions totalled $1.1 billion. The proportions owed by each municipality are set by regulation, and Toronto’s share is just under half a billion. The proportions assessed to each region have not changed since this charge was instituted although one could argue that population shifts and the focus of GO expansion would suggest a different ratio is in order.

Toronto does not carry an account payable for this amount on its books. Meanwhile, in every financial statement, there is a note in this format:

Metrolinx realized a shortfall in municipal funding related to its capital program. The Province has provided funding to bridge the shortfall in the current year in the amount of $141,097 (2015 – $171,111) and the cumulative amount is $1,114,484 (2015 – $973,387). The Province will work with its municipal partners to address the funding shortfalls. [Note 12 to Metrolinx Draft Financial Statements for the year ended March 31, 2016]

What is unclear is whether Queen’s Park will ever call this debt due, or if it will simply be written off as a provincial contribution to GO expansion.

This charge is intended to recover costs for general GO expansion, and it does not include:

- Chargebacks for works undertaken as part of a provincial project that improve municipal assets such as replacement of water mains or provision of improved streets. This was a major issue for Toronto on the Georgetown South project.

- Charges for the abandoned Scarborough LRT project engineering.

Missing from all of the annual reports is any indication of just which GO projects these contributions aided. Indeed, the amounts are intended to go into the general subsidy pot at GO without being tied to its work with the assumption that everyone benefits from “more GO” in the end.

An ongoing problem with provincial funding is that there are various ways that the gas tax grants now paid to municipalities are clawed back. There has been almost no change in the level of gas tax provided, and the amount coming to Toronto has been sitting at about $160m for many years. (Toronto apportions this partly to capital and partly to operations.) The effective value of this contribution falls due to inflation. If Toronto had actually paid their Metrolinx assessment in recent years, this would have wiped out half of the gas tax grant.

In 2017, the TTC is making provision in its budget for additional costs related to Carbon Taxes. This will further erode the contribution from Ontario.

The combined effect of all this will be that, at some point, all of the provincial contribution via gas tax will be consumed by paybacks under various levies and fees.

In an attempt to illuminate this issue, I posed a series of questions to the Minister of Transportation:

Which projects now underway or planned will trigger additions to this outstanding balance including, but not limited to, such things as:

- Ongoing GO improvements (non-RER)

- GO RER

- LRT and BRT projects

In other words, although Ontario has not actually collected on the receivable, will it continue to grow and, in effect, will municipalities be expected to eventually contribute to “provincial” projects, and at what level?

Many projects do not fit into the classic GO Transit model of serving downtown Toronto. For example, York VIVA BRT, The Hurontario and Hamilton LRTs, and the Toronto Crosstown and Finch LRTs serve a very different travel demand from GO’s rail network.

Will the formula for allocating these costs be changed to reflect the service territory and areas benefiting from the projects where municipalities are expected to make a contribution?

Although Ontario makes significant investments in transit, its budgetary effect at the local level will be offset by chargebacks including:

- The deferred Metrolinx receivable above

- Future costs for Presto which is expected to become self-sufficient and will require increases in service fees to local providers to do so

- Future costs for LRT operations

Starting in FY 2011-2012, there was a large increase in the annual charge added to the receivable, an average of $183m/year over the last five years, of which Toronto is responsible for $81.6m/year. What projects contributed to this charge and what was their total value (in effect, my question is what proportion of these projects was back-charged to the municipalities)?

When I receive a reply to these questions, I will update this article.